Causal Inference - Differences-in-Differences

import pandas as pd

import numpy as np

import random

import statsmodels.api as sm

from sklearn.model_selection import cross_val_score

from sklearn.model_selection import RepeatedKFold

from sklearn.linear_model import Lasso

from sklearn.feature_selection import SelectFromModel

import matplotlib.pyplot as plt

from tqdm import tqdm

import statsmodels.api as sm

import itertools

import copy

random.seed(10)

img_dir = '/Users/ida/Google Drive/Big Data Econometrics/Slides/images/'

def fn_generate_cov(dim,corr):

acc = []

for i in range(dim):

row = np.ones((1,dim)) * corr

row[0][i] = 1

acc.append(row)

return np.concatenate(acc,axis=0)

def fn_generate_multnorm(nobs,corr,nvar):

mu = np.zeros(nvar)

std = (np.abs(np.random.normal(loc = 1, scale = .5,size = (nvar,1))))**(1/2)

# generate random normal distribution

acc = []

for i in range(nvar):

acc.append(np.reshape(np.random.normal(mu[i],std[i],nobs),(nobs,-1)))

normvars = np.concatenate(acc,axis=1)

cov = fn_generate_cov(nvar,corr)

C = np.linalg.cholesky(cov)

Y = np.transpose(np.dot(C,np.transpose(normvars)))

# return (Y,np.round(np.corrcoef(Y,rowvar=False),2))

return Y

def fn_randomize_treatment(N,p=0.5):

treated = random.sample(range(N), round(N*p))

return np.array([(1 if i in treated else 0) for i in range(N)]).reshape([N,1])

def fn_bias_rmse_size(theta0,thetahat,se_thetahat,cval = 1.96):

b = thetahat - theta0

bias = np.mean(b)

rmse = np.sqrt(np.mean(b**2))

tval = b/se_thetahat

size = np.mean(1*(np.abs(tval)>cval))

# note size calculated at true parameter value

return (bias,rmse,size)

def fn_plot_with_ci(n_values,tauhats,tau,lb,ub,caption):

fig = plt.figure(figsize = (10,6))

plt.plot(n_values,tauhats,label = '$\hat{\\tau}$')

plt.xlabel('N')

plt.ylabel('$\hat{\\tau}$')

plt.axhline(y=tau, color='r', linestyle='-',linewidth=1,

label='True $\\tau$={}'.format(tau))

plt.title('{}'.format(caption))

plt.fill_between(n_values, lb, ub,

alpha=0.5, edgecolor='#FF9848', facecolor='#FF9848',label = '95% CI')

plt.legend()

def fn_group_to_ind(vecG,n_g):

"""

Transform group effects vector of length G into an n-length individual effects vector

"""

# g = len(vecG)

# return np.concatenate([np.concatenate([vecG[g] for i in range(n_g)]) for g in range(G)]).\

# reshape([n,1])

return np.array(list(itertools.chain.from_iterable(itertools.repeat(x,n_g) for x in vecG)))

def fn_ind_to_panel(vec,T):

"""

Transform (n x 1) vector of individual specific effect to an (n x T) matrix

"""

return np.concatenate([vec for i in range(T)],axis =1)

def fn_mat_wide_to_long(mat,n,T):

"""

Take (n x T) matrix and output nxT vector with observations for each t stacked on top

"""

return np.concatenate([mat[:,i] for i in range(T)]).reshape([n*T,1])

def fn_create_wide_to_long_df(data,colnames,n,G,T):

"""

Take list of matrices in wide format and output a dataframe in long format

"""

n_g = n/G # number of observations in each group

if n_g.is_integer()==False:

print('Error: n_g is not an integer')

else:

n_g = int(n_g)

group = np.concatenate([fn_group_to_ind(np.array(range(G)).reshape([G,1]),n_g) for i in range(T)])

if len(data)!=len(colnames):

print('Error: number of column names not equal to number of variables')

dataDict = {}

for i in range(len(colnames)):

dataDict[colnames[i]] = fn_mat_wide_to_long(data[i],n,T)[:,0]

dataDict['group'] = group[:,0]+1

dataDict['n'] = 1+np.concatenate([range(n) for i in range(T)])

dataDict['t'] = 1+np.array(list(itertools.chain.from_iterable(itertools.repeat(i,n) for i in range(T))))

return pd.DataFrame(dataDict)

# def fn_generate_grouped_panel(n,G,T,n_treated,treat_start,beta,delta,linear_trend = False):

# n_g = n/G # number of observations in each group

# if n_g.is_integer()==False:

# print('Error: n_g is not an integer')

# else:

# n_g = int(n_g)

# alphaG = np.random.normal(1,1,[G,1]) # (G x 1) group fixed effects

# alpha_i = fn_group_to_ind(alphaG,n_g) # (n x 1)

# treatG = np.zeros([G,1])

# treatG[:n_treated,] = 1

# treat_i = fn_group_to_ind(treatG,n_g) # (n x 1)

# # convert to (n X T)

# if linear_trend==True:

# gamma = np.vstack([np.array(range(T)) for i in range(n)])

# else:

# gamma = np.ones([n,1])*np.random.normal(0,1,[1,T]) # (n x T) # time specific effects

# alpha = fn_ind_to_panel(alpha_i,T)

# treat = fn_ind_to_panel(treat_i,T)

# treat = np.concatenate([0*treat[:,:treat_start],treat[:,treat_start:]],axis = 1)

# sig = (np.random.chisquare(2,[n,1])/4+0.5)**(1/2)

# eps = sig*((np.random.chisquare(2,[n,T])-2)*0.5) # (n x T)

# X = np.concatenate([fn_generate_multnorm(n,.5,1) for i in range(T)],axis =1) # (n x T)

# Y = alpha + gamma + beta*treat + delta*X+eps

# return [Y,alpha,gamma,treat,X]

def fn_plot_dd(dfg,treat_start,fig_name=False):

"""

Plot average outcome Y by group

"""

Yg = dfg[['Y','I','group','t']].groupby(['group','t']).mean().reset_index()

treatStatus = dict(zip(Yg[Yg.t==Yg.t.max()]['group'],Yg[Yg.t==Yg.t.max()]['I']))

fig = plt.figure(figsize = (10,6))

for g in Yg.group.unique():

plt.plot(Yg[Yg.group==g]['t'],Yg[Yg.group==g]['Y'],label = 'treatment={}'.format(int(treatStatus[g])))

plt.axvline(x=treat_start+1,color = 'red')

plt.xlabel('time period')

plt.ylabel('outcome')

plt.legend()

if fig_name:

plt.savefig(img_dir + 'dd1.png')

def fn_within_transformation(dfg,varlist,group_var):

"""

Transform each variable in the varlist using the within transformation to eliminate

the group-fixed effects

"""

dfm = dfg[varlist+[group_var]].groupby([group_var]).mean().\

reset_index().\

rename(columns = {k:'{}_bar'.format(k) for k in varlist})

dfg = dfg.merge(dfm, on = ['group'],how = 'left')

dfg['const'] = 1

for v in varlist:

dfg['{}_w'.format(v)] = dfg[v] - dfg['{}_bar'.format(v)]

return dfg

Statsmodels sandwich variance estimators https://github.com/statsmodels/statsmodels/blob/master/statsmodels/stats/sandwich_covariance.py

1. Generate data

$Y_{it} = W_{it}\tau_{it}+\mu_i+\delta_t+\varepsilon_{it}$

$\varepsilon_{it}^{\left( r\right) }/\sigma_{i}\sim IID\left[\chi^{2}(2)-2\right] /2$

$\sigma_{i}^{2}\sim IID\left[ \chi^{2}(2)/4+0.5\right]$

# def fn_randomize_treatment(N,p=0.5):

N = 11

p = .5

treated = random.sample(range(N), round(N*p))

#

treated

[9, 0, 6, 7, 4, 10]

l1 = list(range(10))

l1

[0, 1, 2, 3, 4, 5, 6, 7, 8, 9]

%%timeit

# add 2 to every element

l2 = []

for el in range(len(l1)):

l2 = l2 + [el+2]

l2

1.23 µs ± 90.1 ns per loop (mean ± std. dev. of 7 runs, 1000000 loops each)

%%timeit

[(i+2) for i in l1]

525 ns ± 5.34 ns per loop (mean ± std. dev. of 7 runs, 1000000 loops each)

np.array([(1 if i in treated else 0) for i in range(N)]).reshape([N,1])

array([[1],

[0],

[0],

[0],

[1],

[0],

[1],

[1],

[0],

[1],

[1]])

n = 1000

T = 2

t_treat = 2# first treatment period

p = 0.5

tau = 2

mu = np.random.normal(1,1,[n,1]) # (n x 1)

sig = (np.random.chisquare(2,[n,1])/4+0.5)**(1/2)

eps = sig*((np.random.chisquare(2,[n,T])-2)*0.5) # (n x T)

# eps = np.random.normal([n,T])

delta = np.ones([n,1])*np.random.normal(0,1,[1,T]) # (n x T)

treat = fn_randomize_treatment(n,p) # (n x 1)

W = np.concatenate([np.zeros([n,t_treat-1]),treat*np.ones([n,T-t_treat+1])],axis = 1)

Y = W*tau+mu+delta+eps

Y.shape

(1000, 2)

# constant, treatment dummy, time period = 2 dummy , interaction of those 2 dummies

vecY = np.concatenate([Y[:,0],Y[:,1]]).reshape(2000,1)

vecW = np.concatenate([W[:,0],W[:,1]]).reshape(2000,1)

vecT = np.concatenate([np.zeros([n,1]),np.ones([n,1])])

vecInt = vecW*vecT

vecConst = np.ones([2000,1])xvars = np.hstack([vecConst,vecW,vecT,vecInt])

mod = sm.OLS(vecY,xvars)

res = mod.fit()

print(res.summary())

(2000, 4)

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.196

Model: OLS Adj. R-squared: 0.195

Method: Least Squares F-statistic: 242.9

Date: Wed, 17 Feb 2021 Prob (F-statistic): 3.68e-95

Time: 16:53:15 Log-Likelihood: -3549.5

No. Observations: 2000 AIC: 7105.

Df Residuals: 1997 BIC: 7122.

Df Model: 2

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 0.6274 0.045 13.889 0.000 0.539 0.716

x1 0.9360 0.045 20.723 0.000 0.847 1.025

x2 -0.4562 0.078 -5.831 0.000 -0.610 -0.303

x3 0.9360 0.045 20.723 0.000 0.847 1.025

==============================================================================

Omnibus: 287.827 Durbin-Watson: 1.943

Prob(Omnibus): 0.000 Jarque-Bera (JB): 671.668

Skew: 0.819 Prob(JB): 1.41e-146

Kurtosis: 5.319 Cond. No. 9.13e+15

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The smallest eigenvalue is 3.7e-29. This might indicate that there are

strong multicollinearity problems or that the design matrix is singular.

Yt

array([[2.07832488, 1.68320036],

[3.45006643, 1.64195153],

[3.85554136, 2.00972155],

[3.49435427, 1.76502504],

[2.33965988, 0.87416435]])

Yt = Y[np.where(treat==1)[0],:] #select rows where the corresponding row in treat = 1

Yc = Y[np.where(treat==0)[0],:]

Yt.shape, Yc.shape

((500, 2), (500, 2))

plt.hist(eps)

plt.title('Distribution of errors')

Text(0.5, 1.0, 'Distribution of errors')

Estimate parameter of interest by running a regression of $\Delta Y_{i1}$ on the treatment indicator and an intercept

Ydiff = Y[:,1]-Y[:,0]

Wmod = copy.deepcopy(W)

Wmod[:,0] = 1

model = sm.OLS(Ydiff,Wmod)

res = model.fit()

res.summary()

| Dep. Variable: | y | R-squared: | 0.328 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.327 |

| Method: | Least Squares | F-statistic: | 487.3 |

| Date: | Mon, 08 Feb 2021 | Prob (F-statistic): | 2.96e-88 |

| Time: | 13:40:23 | Log-Likelihood: | -1780.2 |

| No. Observations: | 1000 | AIC: | 3564. |

| Df Residuals: | 998 | BIC: | 3574. |

| Df Model: | 1 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| const | -0.5229 | 0.064 | -8.140 | 0.000 | -0.649 | -0.397 |

| x1 | 2.0057 | 0.091 | 22.075 | 0.000 | 1.827 | 2.184 |

| Omnibus: | 138.012 | Durbin-Watson: | 1.955 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 959.762 |

| Skew: | 0.403 | Prob(JB): | 3.89e-209 |

| Kurtosis: | 7.731 | Cond. No. | 2.62 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

$Y_{i1} - Y_{i0} = \mu_i + ……. - (\mu_i + …….)$

Yt_diff = np.mean(Yt[:,1])-np.mean(Yt[:,0]) # eliminates mu_i

Yc_diff = np.mean(Yc[:,1])-np.mean(Yc[:,0]) # eliminates mu_i

Yt_diff - Yc_diff # eliminates the delta_t

2.0056559437520955

v_Y = np.concatenate([Y[:,i] for i in range(T)]).reshape([2*n,1])

# v_W = np.concatenate([W[:,i] for i in range(T)]).reshape([2*n,1])

v_W = np.concatenate([W[:,1] for i in range(T)]).reshape([2*n,1])

v_mu = np.concatenate([mu for i in range(T)])

v_n = np.concatenate([range(1,n+1) for i in range(T)]).reshape([2*n,1])

v_t = np.concatenate([i*np.ones([n,1]) for i in range(1,T+1)])

df = pd.DataFrame({'y':v_Y[:,0],

'W':v_W[:,0],

'mu':v_mu[:,0],

'n':v_n[:,0],

't':v_t[:,0]})

Now let $T_i = 1$ if $t=2$ and $T_i=0$ otherwise and run regression

$Y_i = \alpha+W_{i1}+T_i+W_{i1}*T_i$

df['Ti'] = 1*(df.t==2)

df['const'] = 1

df['int'] = df.W*df.Ti

mod = sm.OLS(df.y,df[['const','W','Ti','int']])

res = mod.fit()

res.summary()

| Dep. Variable: | y | R-squared: | 0.212 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.211 |

| Method: | Least Squares | F-statistic: | 179.4 |

| Date: | Mon, 08 Feb 2021 | Prob (F-statistic): | 5.26e-103 |

| Time: | 13:40:24 | Log-Likelihood: | -3550.4 |

| No. Observations: | 2000 | AIC: | 7109. |

| Df Residuals: | 1996 | BIC: | 7131. |

| Df Model: | 3 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| const | 0.6379 | 0.064 | 9.978 | 0.000 | 0.512 | 0.763 |

| W | -0.0210 | 0.090 | -0.232 | 0.816 | -0.198 | 0.156 |

| Ti | -0.5229 | 0.090 | -5.785 | 0.000 | -0.700 | -0.346 |

| int | 2.0057 | 0.128 | 15.687 | 0.000 | 1.755 | 2.256 |

| Omnibus: | 295.177 | Durbin-Watson: | 1.945 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 702.857 |

| Skew: | 0.831 | Prob(JB): | 2.38e-153 |

| Kurtosis: | 5.381 | Cond. No. | 6.85 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Let’s focus on the more interesting case where we observe multiple time periods and multiple groups

$Y_{igt} = \alpha_g+\gamma_t+\beta I_{gt}+\delta X_{igt}+\varepsilon_{igt}$

Assessing DD identification the key identifying assumption in DD models is that the treatment states/groups (g) have similar trends to the control states in the absence of treatment

def fn_generate_grouped_panel(n,G,T,n_treated,treat_start,beta,delta,linear_trend = False,corr = False):

n_g = n/G # number of observations in each group

if n_g.is_integer()==False:

return print('Error: n_g is not an integer')

else:

n_g = int(n_g)

alphaG = np.random.normal(1,1,[G,1]) # (G x 1) group fixed effects

alpha_i = fn_group_to_ind(alphaG,n_g) # (n x 1)

treatG = np.zeros([G,1])

treatG[:n_treated,] = 1

treat_i = fn_group_to_ind(treatG,n_g) # (n x 1)

# convert to (n X T)

if linear_trend==True:

gamma = np.vstack([np.array(range(T)) for i in range(n)])

else:

gamma = np.ones([n,1])*np.random.normal(0,1,[1,T]) # (n x T) # time specific effects

alpha = fn_ind_to_panel(alpha_i,T)

treat = fn_ind_to_panel(treat_i,T)

treat = np.concatenate([0*treat[:,:treat_start],treat[:,treat_start:]],axis = 1)

sig = (np.random.chisquare(2,[n,1])/4+0.5)**(1/2)

eps = sig*((np.random.chisquare(2,[n,T])-2)*0.5) # (n x T)

if corr == True:

rho = .7

u = np.zeros(eps.shape)

u[:,0] = eps[:,0]

for t in range(1,T):

u[:,t] = rho*u[:,t-1]+eps[:,t]

X = np.concatenate([fn_generate_multnorm(n,.5,1) for i in range(T)],axis =1) # (n x T)

if corr == False:

Y = alpha + gamma + beta*treat + delta*X+eps

else:

Y = alpha + gamma + beta*treat + delta*X + u

return [Y,alpha,gamma,treat,X]

# def fn_generate_grouped_panel(n,G,T,n_treated,treat_start,beta,delta,linear_trend = False,corr = False):

n = 10

G = 2

T = 5

n_treated = 1

treat_start = 4

beta = 1

delta = .5

linear_trend = True

n_g = n/G # number of observations in each group

if n_g.is_integer()==False:

print('Error: n_g is not an integer')

n_g = int(n_g)

alphaG = np.random.normal(1,1,[G,1]) # (G x 1) group fixed effects

alpha_i = fn_group_to_ind(alphaG,n_g) # (n x 1)

treatG = np.zeros([G,1])

treatG[:n_treated,] = 1

treat_i = fn_group_to_ind(treatG,n_g) # (n x 1)

treat_i,treatG

(array([[1.],

[1.],

[1.],

[1.],

[1.],

[0.],

[0.],

[0.],

[0.],

[0.]]),

array([[1.],

[0.]]))

gamma = np.ones([n,1])*np.random.normal(0,1,[1,T])

gamma

array([[ 0.53272734, 0.51828703, -0.48633918, -1.74128078, -2.98146079],

[ 0.53272734, 0.51828703, -0.48633918, -1.74128078, -2.98146079],

[ 0.53272734, 0.51828703, -0.48633918, -1.74128078, -2.98146079],

[ 0.53272734, 0.51828703, -0.48633918, -1.74128078, -2.98146079],

[ 0.53272734, 0.51828703, -0.48633918, -1.74128078, -2.98146079],

[ 0.53272734, 0.51828703, -0.48633918, -1.74128078, -2.98146079],

[ 0.53272734, 0.51828703, -0.48633918, -1.74128078, -2.98146079],

[ 0.53272734, 0.51828703, -0.48633918, -1.74128078, -2.98146079],

[ 0.53272734, 0.51828703, -0.48633918, -1.74128078, -2.98146079],

[ 0.53272734, 0.51828703, -0.48633918, -1.74128078, -2.98146079]])

Serially corellated errors:

$u_t = \rho*u_{t-1}+e_t$

# convert to (n X T)

if linear_trend==True:

gamma = np.vstack([np.array(range(T)) for i in range(n)])

else:

gamma = np.ones([n,1])*np.random.normal(0,1,[1,T]) # (n x T) # time specific effects

alpha = fn_ind_to_panel(alpha_i,T)

treat = fn_ind_to_panel(treat_i,T)

treat = np.concatenate([0*treat[:,:treat_start],treat[:,treat_start:]],axis = 1)

sig = (np.random.chisquare(2,[n,1])/4+0.5)**(1/2)

eps = sig*((np.random.chisquare(2,[n,T])-2)*0.5) # (n x T)

if corr == True:

rho = .7

u = np.zeros(eps.shape)

u[:,0] = eps[:,0]

for t in range(1,T):

u[:,t] = rho*u[:,t-1]+eps[:,t]

X = np.concatenate([fn_generate_multnorm(n,.5,1) for i in range(T)],axis =1) # (n x T)

alpha.shape, gamma.shape, treat.shape

((10, 5), (10, 5), (10, 5))

treat

array([[0., 0., 0., 0., 1.],

[0., 0., 0., 0., 1.],

[0., 0., 0., 0., 1.],

[0., 0., 0., 0., 1.],

[0., 0., 0., 0., 1.],

[0., 0., 0., 0., 0.],

[0., 0., 0., 0., 0.],

[0., 0., 0., 0., 0.],

[0., 0., 0., 0., 0.],

[0., 0., 0., 0., 0.]])

if corr == False:

Y = alpha + gamma + beta*treat + delta*X+eps

else:

Y = alpha + gamma + beta*treat + delta*X + u

return [Y,alpha,gamma,treat,X]

File "<ipython-input-207-64a684190739>", line 6

return [Y,alpha,gamma,treat,X]

^

SyntaxError: 'return' outside function

$Y_{igt} = \alpha_g+\gamma_t+\beta I_{gt}+\delta X_{igt}+\varepsilon_{igt}$

Within transformation to get rid of $\alpha_g$:

$Y_{igt} - \bar{Y}_{gt}$

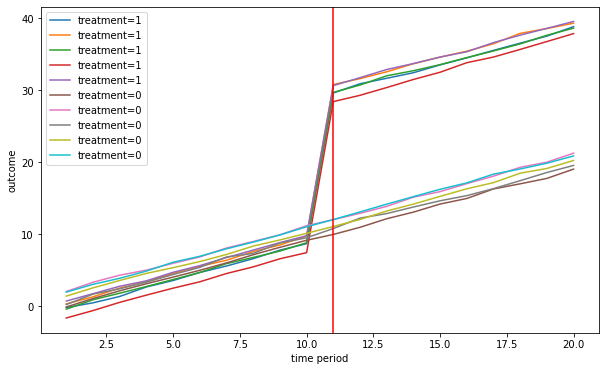

n = 2 # 2 units and 1 unit is in each group

G = 2

n_treated = 1

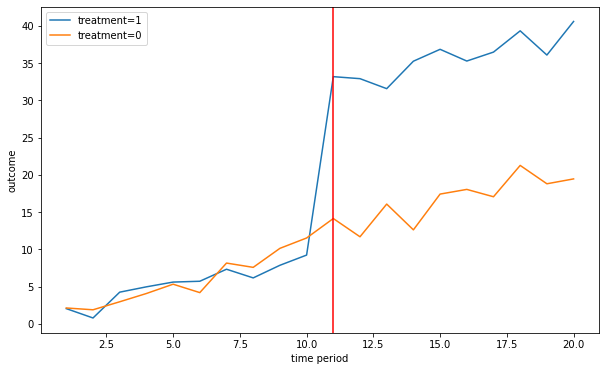

T = 20

beta = 20

delta = 1

treat_start = 10 # when treatment starts

Plot the outcome for the treatment and control group

linear_trend = True

[Y,alpha,gamma,treat,X]= fn_generate_grouped_panel(n,G,T,n_treated,treat_start,beta,delta,linear_trend)

colnames = ['Y','alpha','gamma','I','X']

data = [Y,alpha,gamma,treat,X]

dfg = fn_create_wide_to_long_df(data,colnames,n,G,T)

fn_plot_dd(dfg,treat_start)

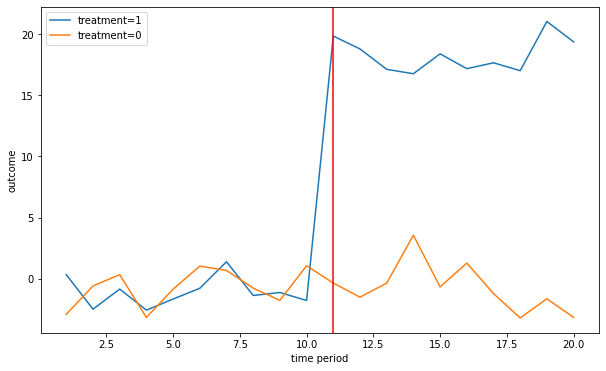

linear_trend = False

[Y,alpha,gamma,treat,X]= fn_generate_grouped_panel(n,G,T,n_treated,treat_start,beta,delta,linear_trend)

colnames = ['Y','alpha','gamma','I','X']

data = [Y,alpha,gamma,treat,X]

dfg = fn_create_wide_to_long_df(data,colnames,n,G,T)

fn_plot_dd(dfg,treat_start)

Estimation

data = [Y,alpha,gamma,treat,X]

colnames = ['Y','alpha','gamma','I','X']

dfg = fn_create_wide_to_long_df(data,colnames,n,G,T)

dfg = fn_within_transformation(dfg,colnames,'group')

dfg.head()

| Y | alpha | gamma | I | X | group | n | t | Y_bar | alpha_bar | gamma_bar | I_bar | X_bar | const | Y_w | alpha_w | gamma_w | I_w | X_w | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.319496 | -0.895547 | -0.546378 | 0.0 | 1.377812 | 1 | 1 | 1 | 8.615999 | -0.895547 | -0.162203 | 0.5 | -0.15752 | 1 | -8.296503 | -2.220446e-16 | -0.384175 | -0.5 | 1.535332 |

| 1 | -2.919256 | -0.286708 | -0.546378 | 0.0 | -1.078144 | 2 | 2 | 1 | -0.720491 | -0.286708 | -0.162203 | 0.0 | -0.04039 | 1 | -2.198765 | -1.110223e-16 | -0.384175 | 0.0 | -1.037754 |

| 2 | -2.500770 | -0.895547 | -0.513985 | 0.0 | 0.332036 | 1 | 1 | 2 | 8.615999 | -0.895547 | -0.162203 | 0.5 | -0.15752 | 1 | -11.116769 | -2.220446e-16 | -0.351782 | -0.5 | 0.489555 |

| 3 | -0.600016 | -0.286708 | -0.513985 | 0.0 | 1.036672 | 2 | 2 | 2 | -0.720491 | -0.286708 | -0.162203 | 0.0 | -0.04039 | 1 | 0.120474 | -1.110223e-16 | -0.351782 | 0.0 | 1.077062 |

| 4 | -0.856377 | -0.895547 | 1.264813 | 0.0 | -0.665249 | 1 | 1 | 3 | 8.615999 | -0.895547 | -0.162203 | 0.5 | -0.15752 | 1 | -9.472376 | -2.220446e-16 | 1.427016 | -0.5 | -0.507730 |

Estimation using a full set of time and group dummies

# pd.get_dummies(dfg.group)

xvars = pd.concat([dfg[['I','X']],

pd.get_dummies(dfg['group'],drop_first = False),

pd.get_dummies(dfg['t'],drop_first = False)],axis = 1)

mod = sm.OLS(dfg['Y'],xvars)

res = mod.fit()

res.summary()

| Dep. Variable: | Y | R-squared: | 0.992 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.981 |

| Method: | Least Squares | F-statistic: | 93.89 |

| Date: | Mon, 08 Feb 2021 | Prob (F-statistic): | 1.06e-13 |

| Time: | 13:40:33 | Log-Likelihood: | -45.914 |

| No. Observations: | 40 | AIC: | 137.8 |

| Df Residuals: | 17 | BIC: | 176.7 |

| Df Model: | 22 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| I | 20.4001 | 0.767 | 26.582 | 0.000 | 18.781 | 22.019 |

| X | 1.2694 | 0.277 | 4.576 | 0.000 | 0.684 | 1.855 |

| 1 | -1.2907 | 0.436 | -2.959 | 0.009 | -2.211 | -0.370 |

| 2 | -0.5759 | 0.251 | -2.296 | 0.035 | -1.105 | -0.047 |

| 1 | -0.5568 | 0.824 | -0.676 | 0.508 | -2.295 | 1.182 |

| 2 | -1.4858 | 0.841 | -1.767 | 0.095 | -3.260 | 0.288 |

| 3 | 1.1783 | 0.834 | 1.412 | 0.176 | -0.582 | 2.939 |

| 4 | -0.1733 | 0.920 | -0.189 | 0.853 | -2.113 | 1.767 |

| 5 | -1.3141 | 0.846 | -1.554 | 0.139 | -3.099 | 0.471 |

| 6 | 1.8082 | 0.845 | 2.141 | 0.047 | 0.026 | 3.590 |

| 7 | 1.6278 | 0.825 | 1.972 | 0.065 | -0.113 | 3.369 |

| 8 | -0.1100 | 0.824 | -0.134 | 0.895 | -1.849 | 1.629 |

| 9 | -0.6017 | 0.824 | -0.730 | 0.475 | -2.339 | 1.136 |

| 10 | 0.5768 | 0.824 | 0.700 | 0.493 | -1.162 | 2.315 |

| 11 | 0.4581 | 0.836 | 0.548 | 0.591 | -1.305 | 2.221 |

| 12 | 0.2653 | 0.839 | 0.316 | 0.756 | -1.505 | 2.035 |

| 13 | -0.1689 | 0.835 | -0.202 | 0.842 | -1.930 | 1.592 |

| 14 | 1.6129 | 0.835 | 1.932 | 0.070 | -0.148 | 3.374 |

| 15 | -0.8069 | 0.848 | -0.951 | 0.355 | -2.596 | 0.983 |

| 16 | 1.4182 | 0.864 | 1.641 | 0.119 | -0.405 | 3.242 |

| 17 | -0.6037 | 0.831 | -0.726 | 0.478 | -2.358 | 1.150 |

| 18 | -2.1873 | 0.832 | -2.628 | 0.018 | -3.943 | -0.431 |

| 19 | -1.4659 | 0.968 | -1.514 | 0.148 | -3.509 | 0.577 |

| 20 | -1.3379 | 0.840 | -1.593 | 0.130 | -3.109 | 0.434 |

| Omnibus: | 4.798 | Durbin-Watson: | 2.930 |

|---|---|---|---|

| Prob(Omnibus): | 0.091 | Jarque-Bera (JB): | 5.432 |

| Skew: | 0.000 | Prob(JB): | 0.0661 |

| Kurtosis: | 4.805 | Cond. No. | 2.05e+16 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The smallest eigenvalue is 9.41e-32. This might indicate that there are

strong multicollinearity problems or that the design matrix is singular.

Estimation using a within group transformation

_w denotes variables that come out of the within transformation

xvars = pd.concat([dfg[['I_w','X_w']],

pd.get_dummies(dfg['t'])],axis = 1)

mod = sm.OLS(dfg['Y_w'],xvars)

res = mod.fit()

res.summary()

| Dep. Variable: | Y_w | R-squared: | 0.988 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.975 |

| Method: | Least Squares | F-statistic: | 72.02 |

| Date: | Mon, 08 Feb 2021 | Prob (F-statistic): | 2.62e-13 |

| Time: | 13:40:34 | Log-Likelihood: | -45.914 |

| No. Observations: | 40 | AIC: | 135.8 |

| Df Residuals: | 18 | BIC: | 173.0 |

| Df Model: | 21 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| I_w | 20.4001 | 0.746 | 27.352 | 0.000 | 18.833 | 21.967 |

| X_w | 1.2694 | 0.270 | 4.709 | 0.000 | 0.703 | 1.836 |

| 1 | -0.4634 | 0.824 | -0.563 | 0.581 | -2.194 | 1.267 |

| 2 | -1.3925 | 0.839 | -1.659 | 0.114 | -3.156 | 0.371 |

| 3 | 1.2716 | 0.834 | 1.525 | 0.145 | -0.481 | 3.024 |

| 4 | -0.0800 | 0.915 | -0.087 | 0.931 | -2.003 | 1.843 |

| 5 | -1.2208 | 0.844 | -1.446 | 0.165 | -2.994 | 0.553 |

| 6 | 1.9015 | 0.844 | 2.253 | 0.037 | 0.129 | 3.674 |

| 7 | 1.7212 | 0.825 | 2.086 | 0.051 | -0.012 | 3.455 |

| 8 | -0.0167 | 0.824 | -0.020 | 0.984 | -1.748 | 1.715 |

| 9 | -0.5083 | 0.824 | -0.617 | 0.545 | -2.239 | 1.222 |

| 10 | 0.6701 | 0.824 | 0.813 | 0.427 | -1.061 | 2.401 |

| 11 | 0.5514 | 0.828 | 0.666 | 0.514 | -1.187 | 2.290 |

| 12 | 0.3586 | 0.831 | 0.431 | 0.671 | -1.388 | 2.105 |

| 13 | -0.0755 | 0.827 | -0.091 | 0.928 | -1.813 | 1.662 |

| 14 | 1.7062 | 0.827 | 2.063 | 0.054 | -0.031 | 3.444 |

| 15 | -0.7136 | 0.839 | -0.850 | 0.406 | -2.477 | 1.050 |

| 16 | 1.5116 | 0.856 | 1.766 | 0.094 | -0.286 | 3.310 |

| 17 | -0.5103 | 0.824 | -0.619 | 0.543 | -2.241 | 1.220 |

| 18 | -2.0940 | 0.825 | -2.540 | 0.021 | -3.826 | -0.362 |

| 19 | -1.3726 | 0.954 | -1.439 | 0.167 | -3.376 | 0.631 |

| 20 | -1.2445 | 0.831 | -1.497 | 0.152 | -2.991 | 0.502 |

| Omnibus: | 4.798 | Durbin-Watson: | 2.930 |

|---|---|---|---|

| Prob(Omnibus): | 0.091 | Jarque-Bera (JB): | 5.432 |

| Skew: | 0.000 | Prob(JB): | 0.0661 |

| Kurtosis: | 4.805 | Cond. No. | 7.06 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

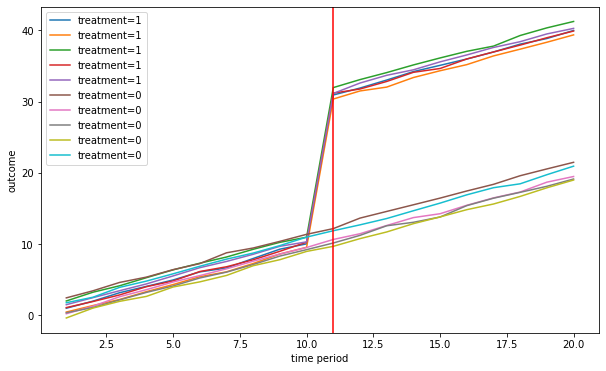

Multiple groups and time periods

$Y_{igt} = \alpha_g+\gamma_t+\beta I_{gt}+\delta X_{igt}+\varepsilon_{igt}$

n = 1000

G = 10

n_treated = 5

T = 20

beta = 20

delta = 1

treat_start = 10

linear_trend = True

[Y,alpha,gamma,treat,X]= fn_generate_grouped_panel(n,G,T,n_treated,treat_start,beta,delta,linear_trend)

colnames = ['Y','alpha','gamma','I','X']

data = [Y,alpha,gamma,treat,X]

dfg = fn_create_wide_to_long_df(data,colnames,n,G,T)

fn_plot_dd(dfg,treat_start)

# dfg.head()

Estimation

dfw = fn_within_transformation(dfg,colnames,'group')

xvars = pd.concat([dfw[['I_w','X_w']],

pd.get_dummies(dfw['t'])],axis = 1)

mod = sm.OLS(dfw['Y_w'],xvars,cluster= dfw['group'])

res = mod.fit(cov_type='HC1')

t = res.params.I_w/res.HC1_se.I_w

res.summary()

| Dep. Variable: | Y_w | R-squared: | 0.993 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.993 |

| Method: | Least Squares | F-statistic: | nan |

| Date: | Mon, 08 Feb 2021 | Prob (F-statistic): | nan |

| Time: | 13:40:36 | Log-Likelihood: | -28192. |

| No. Observations: | 20000 | AIC: | 5.643e+04 |

| Df Residuals: | 19978 | BIC: | 5.660e+04 |

| Df Model: | 21 | ||

| Covariance Type: | HC1 |

| coef | std err | z | P>|z| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| I_w | 19.9867 | 0.028 | 712.870 | 0.000 | 19.932 | 20.042 |

| X_w | 0.9981 | 0.007 | 147.009 | 0.000 | 0.985 | 1.011 |

| 1 | -9.5285 | 0.032 | -294.481 | 0.000 | -9.592 | -9.465 |

| 2 | -8.5477 | 0.031 | -278.041 | 0.000 | -8.608 | -8.487 |

| 3 | -7.4749 | 0.032 | -233.314 | 0.000 | -7.538 | -7.412 |

| 4 | -6.5301 | 0.031 | -213.574 | 0.000 | -6.590 | -6.470 |

| 5 | -5.5166 | 0.031 | -178.651 | 0.000 | -5.577 | -5.456 |

| 6 | -4.4325 | 0.034 | -130.609 | 0.000 | -4.499 | -4.366 |

| 7 | -3.5591 | 0.030 | -116.873 | 0.000 | -3.619 | -3.499 |

| 8 | -2.5156 | 0.032 | -77.789 | 0.000 | -2.579 | -2.452 |

| 9 | -1.4233 | 0.034 | -41.344 | 0.000 | -1.491 | -1.356 |

| 10 | -0.4743 | 0.032 | -14.866 | 0.000 | -0.537 | -0.412 |

| 11 | 0.4865 | 0.032 | 15.107 | 0.000 | 0.423 | 0.550 |

| 12 | 1.5096 | 0.033 | 46.048 | 0.000 | 1.445 | 1.574 |

| 13 | 2.4724 | 0.031 | 78.889 | 0.000 | 2.411 | 2.534 |

| 14 | 3.5285 | 0.031 | 112.952 | 0.000 | 3.467 | 3.590 |

| 15 | 4.4621 | 0.030 | 148.465 | 0.000 | 4.403 | 4.521 |

| 16 | 5.5001 | 0.032 | 170.856 | 0.000 | 5.437 | 5.563 |

| 17 | 6.5112 | 0.032 | 204.902 | 0.000 | 6.449 | 6.574 |

| 18 | 7.5147 | 0.035 | 215.853 | 0.000 | 7.446 | 7.583 |

| 19 | 8.4975 | 0.034 | 246.447 | 0.000 | 8.430 | 8.565 |

| 20 | 9.5200 | 0.031 | 308.540 | 0.000 | 9.460 | 9.580 |

| Omnibus: | 9425.670 | Durbin-Watson: | 2.007 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 68273.339 |

| Skew: | 2.146 | Prob(JB): | 0.00 |

| Kurtosis: | 10.969 | Cond. No. | 7.40 |

Notes:

[1] Standard Errors are heteroscedasticity robust (HC1)

Simulate placebo policy

def fn_placebo_treatment(row,tstart,treated):

if (row.t>=tstart) & (row.group in treated):

return 1

else:

return 0

THIS IS THE PART WE DIDN’T COVER IN LECTURE 4

What the code below does is to simulate a placebo policy - where we mistakenly treat some units as being assigned a treatment even though they’re not and we estiamte the treatment effect We expect to reject the null hypothesis that the treatment effect is different from 0 a low % of the time because the treatment effect doesn’t exist so it is zero! Indeed, we reject the null around 1% of the time below. With more replications it should converge to 5%.

R = 100

l = []

n = 1000

G = 10

n_treated = 0

T = 20

beta = 20

delta = 1

treat_start = 10

linear_trend = True

colnames = ['Y','alpha','gamma','I','X']

for r in tqdm(range(R)):

np.random.seed(r)

[Y,alpha,gamma,treat,X]= fn_generate_grouped_panel(n,G,T,n_treated,treat_start,beta,delta,linear_trend)

data = [Y,alpha,gamma,treat,X]

dfg = fn_create_wide_to_long_df(data,colnames,n,G,T)

tstart = random.choice(range(dfg.t.min(),dfg.t.max()+1)) # treatment start date

treated = random.choices(range(dfg.group.min(),dfg.group.max()+1),k = int(dfg.group.max()/2))

dfg['I'] = dfg.apply(lambda row: fn_placebo_treatment(row,tstart,treated),axis = 1)

dfw = fn_within_transformation(dfg,colnames,'group')

xvars = pd.concat([dfw[['I_w','X_w']],

pd.get_dummies(dfw['t'])],axis = 1)

mod = sm.OLS(dfw['Y_w'],xvars,cluster= dfw['group'])

res = mod.fit(cov_type='HC1')

t = res.params.I_w/res.HC1_se.I_w

if np.abs(t)>1.96:

l = l+[1]

else:

l = l+[0]

6%|▌ | 6/100 [00:02<00:35, 2.61it/s]<ipython-input-223-02feb1c08ec8>:27: RuntimeWarning: invalid value encountered in double_scalars

t = res.params.I_w/res.HC1_se.I_w

100%|██████████| 100/100 [00:32<00:00, 3.11it/s]

np.mean(l) # we reject the null of a nonzero treatment effect 1% of the time

0.01

Now let’s add some serial correlation to the DGP

n = 1000

G = 10

n_treated = 5

T = 20

beta = 20

delta = 1

treat_start = 10

linear_trend = True

serial_corr = True

[Y,alpha,gamma,treat,X]= fn_generate_grouped_panel(n,G,T,n_treated,treat_start,beta,delta,linear_trend,serial_corr)

colnames = ['Y','alpha','gamma','I','X']

data = [Y,alpha,gamma,treat,X]

dfg = fn_create_wide_to_long_df(data,colnames,n,G,T)

fn_plot_dd(dfg,treat_start)

$y_{it}$

shock at time $t$ equal to $\gamma_t$

Estimate:

$y_{it} = \alpha + \beta*\gamma_t+\varepsilon_{it}$

Obtain residuals $\hat{\varepsilon}_{it}$

def fn_run_mc(beta,R,corr):

l0 = []

l1 = []

for r in tqdm(range(R)):

np.random.seed(r)

[Y,alpha,gamma,treat,X]= fn_generate_grouped_panel(n,G,T,n_treated,treat_start,beta,delta,linear_trend,corr)

data = [Y,alpha,gamma,treat,X]

dfg = fn_create_wide_to_long_df(data,colnames,n,G,T)

tstart = random.choice(range(dfg.t.min(),dfg.t.max()+1))

treated = random.choices(range(dfg.group.min(),dfg.group.max()+1),k = int(dfg.group.max()/2))

# dfg['I'] = dfg.apply(lambda row: fn_placebo_treatment(row,tstart,treated),axis = 1)

dfw = fn_within_transformation(dfg,colnames,'group')

xvars = pd.concat([dfw[['I_w','X_w']],

pd.get_dummies(dfw['t'])],axis = 1)

mod = sm.OLS(dfw['Y_w'],xvars,cluster= dfw['group'])

res = mod.fit(cov_type='HC1')

t0 = res.params.I_w/res.HC1_se.I_w # test H0: beta=0

t1 = (res.params.I_w-beta)/res.HC1_se.I_w # test H0: beta = beta_true

l0 = l0 + [1*(np.abs(t0)>1.96)]

l1 = l1 + [1*(np.abs(t1)>1.96)]

return np.mean(l0),np.mean(l1)

t_stat = .2

t_stat>1.96, 1*(t_stat>1.96)

(False, 0)

R = 500

n = 1000

G = 10

n_treated = 5

T = 20

delta = 1

treat_start = 10

linear_trend = True

colnames = ['Y','alpha','gamma','I','X']

Treatment effect = 2 with no serial correlation

beta = 2

corr = False

h1, hb = fn_run_mc(beta,R,corr)

h1,hb

100%|██████████| 500/500 [00:38<00:00, 13.04it/s]

(1.0, 0.066)

Treatment effect = 2 with serial correlation

beta = 2

corr = True

h1, hb = fn_run_mc(beta,R,corr)

h1,hb

100%|██████████| 500/500 [00:25<00:00, 19.81it/s]

(1.0, 0.34)

Treatment effect = 0, no serial correlation

beta = 0

corr = False

h1, hb = fn_run_mc(beta,R,corr)

print('We reject beta=0 {} of the time'.format(h1))

100%|██████████| 500/500 [00:27<00:00, 18.02it/s]

We reject beta=0 0.066% of the time

Treatment effect = 0, serial correlation

beta = 0

corr = True

h1, hb = fn_run_mc(beta,R,corr)

print('We reject beta=0 {} of the time'.format(h1))

100%|██████████| 500/500 [00:37<00:00, 13.47it/s]

We reject beta=0 0.34 of the time

Sentsitivity tests

Redo the analysis on pre-event years - the estiamted treatment effect should be zero! Are treatment and control gropus similar along observable dimensions? Make sure the change is concentrated around the event Make sure tha tother outcome variables that should be unaffected by the event are indeed unaffected