Causal Inference - Instrumental Variables & Regression Discontinuity

def fn_tauhat_means(Yt,Yc):

nt = len(Yt)

nc = len(Yc)

tauhat = np.mean(Yt)-np.mean(Yc)

se_tauhat = (np.var(Yt,ddof=1)/nt+np.var(Yc,ddof=1)/nc)**(1/2)

return (tauhat,se_tauhat)

def fn_bias_rmse_size(theta0,thetahat,se_thetahat,cval = 1.96):

b = thetahat - theta0

bias = np.mean(b)

rmse = np.sqrt(np.mean(b**2))

tval = b/se_thetahat

size = np.mean(1*(np.abs(tval)>cval))

# note size calculated at true parameter value

return (bias,rmse,size)

def fn_run_experiments(tau,Nrange,p,p0,corr,conf,flagX=False):

n_values = []

tauhats = []

sehats = []

lb = []

ub = []

for N in tqdm(Nrange):

n_values = n_values + [N]

if flagX==False:

Yexp,T = fn_generate_data(tau,N,p,p0,corr,conf,flagX)

Yt = Yexp[np.where(T==1)[0],:]

Yc = Yexp[np.where(T==0)[0],:]

tauhat,se_tauhat = fn_tauhat_means(Yt,Yc)

elif flagX==1:

# use the right covariates in regression

Yexp,T,X = fn_generate_data(tau,N,p,p0,corr,conf,flagX)

Xobs = X[:,:p0]

covars = np.concatenate([T,Xobs],axis = 1)

mod = sm.OLS(Yexp,covars)

res = mod.fit()

tauhat = res.params[0]

se_tauhat = res.HC1_se[0]

elif flagX==2:

# use some of the right covariates and some "wrong" ones

Yexp,T,X = fn_generate_data(tau,N,p,p0,corr,conf,flagX)

Xobs1 = X[:,:np.int(p0/2)]

Xobs2 = X[:,-np.int(p0/2):]

covars = np.concatenate([T,Xobs1,Xobs2],axis = 1)

mod = sm.OLS(Yexp,covars)

res = mod.fit()

tauhat = res.params[0]

se_tauhat = res.HC1_se[0]

tauhats = tauhats + [tauhat]

sehats = sehats + [se_tauhat]

lb = lb + [tauhat-1.96*se_tauhat]

ub = ub + [tauhat+1.96*se_tauhat]

return (n_values,tauhats,sehats,lb,ub)

def fn_plot_with_ci(n_values,tauhats,tau,lb,ub,caption):

fig = plt.figure(figsize = (10,6))

plt.plot(n_values,tauhats,label = '$\hat{\\tau}$')

plt.xlabel('N')

plt.ylabel('$\hat{\\tau}$')

plt.axhline(y=tau, color='r', linestyle='-',linewidth=1,

label='True $\\tau$={}'.format(tau))

plt.title('{}'.format(caption))

plt.fill_between(n_values, lb, ub,

alpha=0.5, edgecolor='#FF9848', facecolor='#FF9848',label = '95% CI')

plt.legend()

Inspired by https://github.com/TeconomicsBlog/notebooks/blob/master/PrincipledInstrumentSelection.ipynb

def fn_generate_cov(dim):

acc = []

for i in range(dim):

row = np.ones((1,dim)) * corr

row[0][i] = 1

acc.append(row)

return np.concatenate(acc,axis=0)

def fn_generate_multnorm(nobs,corr,nvar):

mu = np.zeros(nvar)

std = (np.abs(np.random.normal(loc = 1, scale = .5,size = (nvar,1))))**(1/2)

# generate random normal distribution

acc = []

for i in range(nvar):

acc.append(np.reshape(np.random.normal(mu[i],std[i],nobs),(nobs,-1)))

normvars = np.concatenate(acc,axis=1)

cov = fn_generate_cov(nvar)

C = np.linalg.cholesky(cov)

Y = np.transpose(np.dot(C,np.transpose(normvars)))

# return (Y,np.round(np.corrcoef(Y,rowvar=False),2))

return Y

def fn_generate_data(tau,N,p,p0,corr,conf = True,flagX = False):

"""

p0(int): number of covariates with nonzero coefficients

"""

nvar = p+2 # 1 confounder and variable for randomizing treatment

corr = 0.5 # correlation for multivariate normal

if conf==False:

conf_mult = 0 # remove confounder from outcome

allX = fn_generate_multnorm(N,corr,nvar)

W0 = allX[:,0].reshape([N,1]) # variable for RDD assignment

C = allX[:,1].reshape([N,1]) # confounder

X = allX[:,2:] # observed covariates

# Make T a function of the W0's and unobservable (for RDD)

W = W0 + 0.5*C + 3*X[:,0]-6*X[:,1]

# assign treatment based on threshold along W

T = 1*(W>0)

T = fn_randomize_treatment(N) # choose treated units

err = np.random.normal(0,1,[N,1])

beta0 = np.random.normal(5,5,[p,1])

beta0[p0:p] = 0 # sparse model

Yab = tau*T+X@beta0+conf_mult*0.6*C+err

if flagX==False:

return (Yab,T)

else:

return (Yab,T,X)

# regression discontinuity

# W = W0 + 0.5*C+3*X[:,80].reshape([N,1])-6*X[:,81].reshape([N,1])

# treated = 1*(W>0)

# Yrdd = 1.2* treated - 4*W + X@beta0 +0.6*C+err

p = 10

p0 = 5

nvar = p+2 # 1 confounder and variable for randomizing treatment

tau = 1.2

corr = .5

N = 100

allX = fn_generate_multnorm(N,corr,nvar)

W0 = allX[:,0].reshape([N,1]) # variable for RDD assignment

C = allX[:,1].reshape([N,1]) # confounder

X = allX[:,2:] # observed covariates

# Make T a function of the W0's and unobservable (for RDD)

W = W0 + 0.5*C + 3*X[:,0].reshape([N,1])-6*X[:,1].reshape([N,1])

# assign treatment based on threshold along W

T = 1*(W>0)

err = np.random.normal(0,1,[N,1])

beta0 = np.random.normal(5,5,[p,1])

beta0[p0:p] = 0 # sparse model

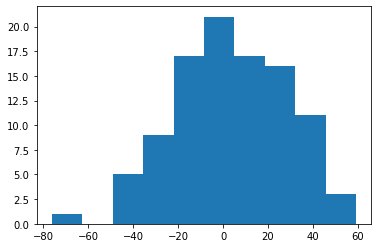

Yrdd = tau*T - 4*W+X@beta0+0.6*C+err

plt.hist(Yrdd)

(array([ 1., 0., 5., 9., 17., 21., 17., 16., 11., 3.]),

array([-76.21997922, -62.67705372, -49.13412822, -35.59120272,

-22.04827722, -8.50535172, 5.03757378, 18.58049928,

32.12342478, 45.66635028, 59.20927578]),

<BarContainer object of 10 artists>)

import pandas as pd

import numpy as np

import random

import statsmodels.api as sm

from sklearn.model_selection import cross_val_score

from sklearn.model_selection import RepeatedKFold

from sklearn.linear_model import Lasso

from sklearn.feature_selection import SelectFromModel

import matplotlib.pyplot as plt

from tqdm import tqdm

import statsmodels.api as sm

import itertools

from linearmodels import IV2SLS, IVLIML, IVGMM, IVGMMCUE

import copy

random.seed(10)

N = 1000

tau = 2

weak = np.random.normal(0,1,[N,1])

good = np.random.normal(0,1,[N,1])

correl = np.random.normal(0,1,[N,1]) # not exognous instrument

C = 3*correl + np.random.normal(0,1,[N,1])

X = -.00001 * np.round(weak) + 2.5 * correl + 2.5 * good + .5 * C + np.random.normal(0,1,[N,1])

Y = tau * X + 1.1 * C + np.random.normal(0,1,[N,1])

df = pd.DataFrame({'Y':Y[:,0],'X':X[:,0],'correl':correl[:,0],'good':good[:,0],'weak':weak[:,0]},index = None)

df.head()

| Y | X | correl | good | weak | |

|---|---|---|---|---|---|

| 0 | -12.972424 | -6.012842 | -0.588808 | -1.657263 | 0.550849 |

| 1 | 23.654806 | 8.116217 | 2.378486 | -0.486845 | -0.912524 |

| 2 | 5.926820 | 1.860624 | 0.441214 | -0.265508 | -1.396208 |

| 3 | -37.769825 | -15.705979 | -2.176071 | -1.956658 | -0.322946 |

| 4 | 17.074535 | 5.607653 | 1.817937 | -0.515070 | -2.358285 |

Naive regression without an instrument

mod = sm.OLS(Y,X)

res = mod.fit()

print(res.summary())

OLS Regression Results

=======================================================================================

Dep. Variable: y R-squared (uncentered): 0.969

Model: OLS Adj. R-squared (uncentered): 0.969

Method: Least Squares F-statistic: 3.135e+04

Date: Fri, 05 Feb 2021 Prob (F-statistic): 0.00

Time: 10:33:19 Log-Likelihood: -2229.1

No. Observations: 1000 AIC: 4460.

Df Residuals: 999 BIC: 4465.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

x1 2.5826 0.015 177.055 0.000 2.554 2.611

==============================================================================

Omnibus: 1.961 Durbin-Watson: 2.015

Prob(Omnibus): 0.375 Jarque-Bera (JB): 1.906

Skew: -0.046 Prob(JB): 0.386

Kurtosis: 3.193 Cond. No. 1.00

==============================================================================

Notes:

[1] R² is computed without centering (uncentered) since the model does not contain a constant.

[2] Standard Errors assume that the covariance matrix of the errors is correctly specified.

estDict = {} # store estimates

estDict['no_instrument'] = (float(res.params),float(res.HC0_se))

estDict

{'no_instrument': (2.582590351934214, 0.014621943546545573)}

We can also use the IV2SLS estimator with no instruments

ivmod = IV2SLS(df.Y, exog = df.X, endog = None, instruments = None)

res_2sls = ivmod.fit()

print(res_2sls.summary)

OLS Estimation Summary

==============================================================================

Dep. Variable: Y R-squared: 0.9689

Estimator: OLS Adj. R-squared: 0.9688

No. Observations: 1000 F-statistic: 3.059e+04

Date: Fri, Feb 12 2021 P-value (F-stat) 0.0000

Time: 15:09:54 Distribution: chi2(1)

Cov. Estimator: robust

Parameter Estimates

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

X 2.6004 0.0149 174.91 0.0000 2.5713 2.6295

==============================================================================

/Users/ida/opt/anaconda3/lib/python3.8/site-packages/linearmodels/iv/data.py:25: FutureWarning: is_categorical is deprecated and will be removed in a future version. Use is_categorical_dtype instead

if is_categorical(s):

Fit using a good instrument (strong first stage and satisfies exclusion restriction)

ivmod = IV2SLS(df.Y, exog = None, endog = df.X, instruments = df.good)

res_2sls = ivmod.fit()

estDict['good_instrument'] = (float(res_2sls.params),float(res_2sls.std_errors))

print(res_2sls.summary)

IV-2SLS Estimation Summary

==============================================================================

Dep. Variable: Y R-squared: 0.9157

Estimator: IV-2SLS Adj. R-squared: 0.9156

No. Observations: 1000 F-statistic: 1645.8

Date: Fri, Feb 12 2021 P-value (F-stat) 0.0000

Time: 15:10:12 Distribution: chi2(1)

Cov. Estimator: robust

Parameter Estimates

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

X 1.9911 0.0491 40.569 0.0000 1.8949 2.0873

==============================================================================

Endogenous: X

Instruments: good

Robust Covariance (Heteroskedastic)

Debiased: False

Fit using a weak instrument (satisfies exclusion restriction)

ivmod = IV2SLS(df.Y, exog = None, endog = df.X, instruments = df.weak)

res_2sls = ivmod.fit()

estDict['weak_instrument'] = (float(res_2sls.params),float(res_2sls.std_errors))

print(res_2sls.summary)

IV-2SLS Estimation Summary

==============================================================================

Dep. Variable: Y R-squared: 0.9623

Estimator: IV-2SLS Adj. R-squared: 0.9623

No. Observations: 1000 F-statistic: 17.369

Date: Fri, Feb 12 2021 P-value (F-stat) 0.0000

Time: 15:10:23 Distribution: chi2(1)

Cov. Estimator: robust

Parameter Estimates

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

X 2.3870 0.5727 4.1677 0.0000 1.2644 3.5096

==============================================================================

Endogenous: X

Instruments: weak

Robust Covariance (Heteroskedastic)

Debiased: False

Fit using an instrument that doesn’t satisfy the exclusion restriction (but with a strong first stage)

Instrument correlated with unobservables

ivmod = IV2SLS(df.Y, exog = None, endog = df.X, instruments = df.correl)

res_2sls = ivmod.fit()

estDict['failed_excl'] = (float(res_2sls.params),float(res_2sls.std_errors))

print(res_2sls.summary)

IV-2SLS Estimation Summary

==============================================================================

Dep. Variable: Y R-squared: 0.9594

Estimator: IV-2SLS Adj. R-squared: 0.9594

No. Observations: 1000 F-statistic: 1.955e+04

Date: Fri, Feb 12 2021 P-value (F-stat) 0.0000

Time: 15:10:58 Distribution: chi2(1)

Cov. Estimator: robust

Parameter Estimates

==============================================================================

Parameter Std. Err. T-stat P-value Lower CI Upper CI

------------------------------------------------------------------------------

X 2.8567 0.0204 139.83 0.0000 2.8166 2.8967

==============================================================================

Endogenous: X

Instruments: correl

Robust Covariance (Heteroskedastic)

Debiased: False

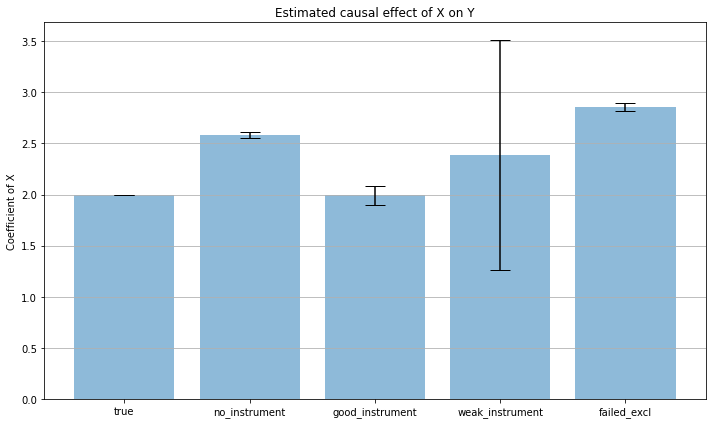

estimates = [tau] + list(i[0] for i in estDict.values())

bnds = [0] + list(1.96*i[1] for i in estDict.values())

x_pos = np.arange(len(estimates))

labels = ['true']+list(estDict.keys())

estDict

{'no_instrument': (2.582590351934214, 0.014621943546545573),

'good_instrument': (1.9910988436149428, 0.04907956766829856),

'weak_instrument': (2.3869998034148607, 0.5727440776150304),

'failed_excl': (2.8566552323095524, 0.02042983578194687)}

labels

['true', 'no_instrument', 'good_instrument', 'weak_instrument', 'failed_excl']

fig, ax = plt.subplots(figsize = (10,6))

ax.bar(x_pos, estimates, yerr=bnds, align='center', alpha=0.5, ecolor='black', capsize=10)

ax.set_ylabel('Coefficient of X')

ax.set_xticks(x_pos)

ax.set_xticklabels(labels)

ax.set_title('Estimated causal effect of X on Y')

ax.yaxis.grid(True)

# Save the figure and show

plt.tight_layout()

# plt.savefig('bar_plot_with_error_bars.png')

plt.show()

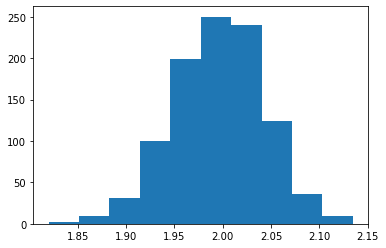

Monte Carlo example

R = 1000

N = 1000

tau = 2

l_weak = []

l_strong = []

for r in tqdm(range(R)):

# generate data

weak = np.random.normal(0,1,[N,1])

good = np.random.normal(0,1,[N,1])

correl = np.random.normal(0,1,[N,1]) # not exognous instrument

C = 3*correl + np.random.normal(0,1,[N,1])

X = -.00001 * np.round(weak) + 2.5 * correl + 2.5 * good + .5 * C + np.random.normal(0,1,[N,1])

Y = tau * X + 1.1 * C + np.random.normal(0,1,[N,1])

df = pd.DataFrame({'Y':Y[:,0],'X':X[:,0],'correl':correl[:,0],'good':good[:,0],'weak':weak[:,0]},index = None)

# estimation with weak instrument

ivmod = IV2SLS(df.Y, exog = None, endog = df.X, instruments = df.weak)

res_2sls = ivmod.fit()

l_weak = l_weak + [float(res_2sls.params)]

# estimation with strong instrument

ivmod = IV2SLS(df.Y, exog = None, endog = df.X, instruments = df.good)

res_2sls = ivmod.fit()

l_strong = l_strong + [float(res_2sls.params)]

100%|██████████| 1000/1000 [00:15<00:00, 66.64it/s]

plt.hist(l_strong)

(array([ 2., 9., 31., 100., 199., 250., 240., 124., 36., 9.]),

array([1.8199192 , 1.85138522, 1.88285125, 1.91431728, 1.9457833 ,

1.97724933, 2.00871536, 2.04018138, 2.07164741, 2.10311344,

2.13457946]),

<BarContainer object of 10 artists>)

np.mean(l_strong)

1.9954114444265139

plt.hist(l_weak)

(array([ 1., 0., 0., 0., 0., 0., 2., 2., 992., 3.]),

array([-707.42250818, -622.92534886, -538.42818953, -453.9310302 ,

-369.43387087, -284.93671155, -200.43955222, -115.94239289,

-31.44523356, 53.05192576, 137.54908509]),

<BarContainer object of 10 artists>)

np.mean(l_weak)

1.6715375931589938

np.quantile(l_weak, q = [.0001,.1, .3, .5, .9, .99])

array([-654.32232836, 0.96837213, 2.26251629, 2.58687549,

4.13499364, 12.34641333])

mylist = [1,2,3]

emptylist = []

for i in range(10):

emptylist = emptylist + [i]

emptylist

[0, 1, 2, 3, 4, 5, 6, 7, 8, 9]