Randomized Experiments

Econ 570 Big Data Econometrics - 2nd TA session

DGP & Monte Carlo Simulation

import pandas as pd

import numpy as np

import random

import statsmodels.api as sm

import matplotlib.pyplot as plt

from tqdm import tqdm

random.seed(10)

# Calculate variance

def fn_variance(data, ddof=0): #ddof: "delta degree of freedom": adjustment to the degrees of freedom for the p-value

n = len(data)

mean = sum(data) / n

return sum((x - mean) ** 2 for x in data) / (n - ddof)

# Note this is equivalent to np.var(Yt,ddof)

# Generate covariance

def fn_generate_cov(dim,corr): #dim : dim X dim matrix with diagonal is 1 and others are corr

acc = []

for i in range(dim):

row = np.ones((1,dim)) * corr

row[0][i] = 1

acc.append(row)

return np.concatenate(acc,axis=0)

corr=0.5

cov=fn_generate_cov(6,corr)

cov

array([[1. , 0.5, 0.5, 0.5, 0.5, 0.5],

[0.5, 1. , 0.5, 0.5, 0.5, 0.5],

[0.5, 0.5, 1. , 0.5, 0.5, 0.5],

[0.5, 0.5, 0.5, 1. , 0.5, 0.5],

[0.5, 0.5, 0.5, 0.5, 1. , 0.5],

[0.5, 0.5, 0.5, 0.5, 0.5, 1. ]])

# Generate multivariate normal distribution

def fn_generate_multnorm(nobs,corr,nvar):

mu = np.zeros(nvar)

std = (np.abs(np.random.normal(loc = 1, scale = .5,size = (nvar,1))))**(1/2)

# generate random normal distribution

acc = []

for i in range(nvar):

acc.append(np.reshape(np.random.normal(mu[i],std[i],nobs),(nobs,-1)))

normvars = np.concatenate(acc,axis=1) # Join a sequence of arrays along an existing axis

cov = fn_generate_cov(nvar,corr) # fn_generate_cov

C = np.linalg.cholesky(cov) # Cholesky decomposition

Y = np.transpose(np.dot(C,np.transpose(normvars)))

# return (Y,np.round(np.corrcoef(Y,rowvar=False),2))

return Y

# Randomly Choose treated unit

def fn_randomize_treatment(N,p=0.5):

treated = random.sample(range(N), round(N*p))

return np.array([(1 if i in treated else 0) for i in range(N)]).reshape([N,1])

# Generate Data (conf: confounder)

def fn_generate_data(tau,N,p,p0,corr,conf = True,flagX = False):

"""

p0(int): number of covariates with nonzero coefficients

"""

nvar = p+2 # 1 confounder and variable for randomizing treatment

corr = 0.5 # correlation for multivariate normal

if conf==False:

conf_mult = 0 # remove confounder from outcome

allX = fn_generate_multnorm(N,corr,nvar) # fn_generate_multnorm

# W0 = allX[:,0].reshape([N,1]) # variable for RDD assignment

C = allX[:,1].reshape([N,1]) # confounder

X = allX[:,2:] # observed covariates

T = fn_randomize_treatment(N) # choose treated units

err = np.random.normal(0,1,[N,1])

beta0 = np.random.normal(5,5,[p,1])

beta0[p0:p] = 0 # sparse model

Yab = tau*T+X@beta0+conf_mult*0.6*C+err

if flagX==False:

return (Yab,T)

else:

return (Yab,T,X)

# regression discontinuity

# W = W0 + 0.5*C+3*X[:,80].reshape([N,1])-6*X[:,81].reshape([N,1])

# treated = 1*(W>0)

# Yrdd = 1.2* treated - 4*W + X@beta0 +0.6*C+err

def fn_tauhat_means(Yt,Yc):

nt = len(Yt)

nc = len(Yc)

tauhat = np.mean(Yt)-np.mean(Yc)

se_tauhat = (np.var(Yt,ddof=1)/nt+np.var(Yc,ddof=1)/nc)**(1/2)

return (tauhat,se_tauhat)

def fn_bias_rmse_size(theta0,thetahat,se_thetahat,cval = 1.96):

b = thetahat - theta0

bias = np.mean(b)

rmse = np.sqrt(np.mean(b**2))

tval = b/se_thetahat

size = np.mean(1*(np.abs(tval)>cval))

# note size calculated at true parameter value

return (bias,rmse,size)

def fn_run_experiments(tau,Nrange,p,p0,corr,conf,flagX=False):

n_values = []

tauhats = []

sehats = []

lb = []

ub = []

for N in tqdm(Nrange):

n_values = n_values + [N]

if flagX==False:

Yexp,T = fn_generate_data(tau,N,p,p0,corr,conf,flagX) # fn_generate_data

Yt = Yexp[np.where(T==1)[0],:]

Yc = Yexp[np.where(T==0)[0],:]

tauhat,se_tauhat = fn_tauhat_means(Yt,Yc) #fn_tauhat_means

elif flagX==1:

# use the right covariates in regression

Yexp,T,X = fn_generate_data(tau,N,p,p0,corr,conf,flagX) # fn_generate_data

Xobs = X[:,:p0]

covars = np.concatenate([T,Xobs],axis = 1)

mod = sm.OLS(Yexp,covars)

res = mod.fit()

tauhat = res.params[0]

se_tauhat = res.HC1_se[0]

elif flagX==2:

# use some of the right covariates and some "wrong" ones

Yexp,T,X = fn_generate_data(tau,N,p,p0,corr,conf,flagX) # fn_generate_data

Xobs1 = X[:,:np.int(p0/2)]

Xobs2 = X[:,-np.int(p0/2):]

covars = np.concatenate([T,Xobs1,Xobs2],axis = 1)

mod = sm.OLS(Yexp,covars)

res = mod.fit()

tauhat = res.params[0]

se_tauhat = res.HC1_se[0]

tauhats = tauhats + [tauhat]

sehats = sehats + [se_tauhat]

lb = lb + [tauhat-1.96*se_tauhat] # lower bound

ub = ub + [tauhat+1.96*se_tauhat] # upper bound

return (n_values,tauhats,sehats,lb,ub)

# Plotting with Confidence Interval

def fn_plot_with_ci(n_values,tauhats,tau,lb,ub,caption):

fig = plt.figure(figsize = (10,6))

plt.plot(n_values,tauhats,label = '$\hat{\\tau}$')

plt.xlabel('N')

plt.ylabel('$\hat{\\tau}$')

plt.axhline(y=tau, color='r', linestyle='-',linewidth=1,

label='True $\\tau$={}'.format(tau))

plt.title('{}'.format(caption))

plt.fill_between(n_values, lb, ub,

alpha=0.5, edgecolor='#FF9848', facecolor='#FF9848',label = '95% CI')

plt.legend()

Statsmodels sandwich variance estimators https://github.com/statsmodels/statsmodels/blob/master/statsmodels/stats/sandwich_covariance.py

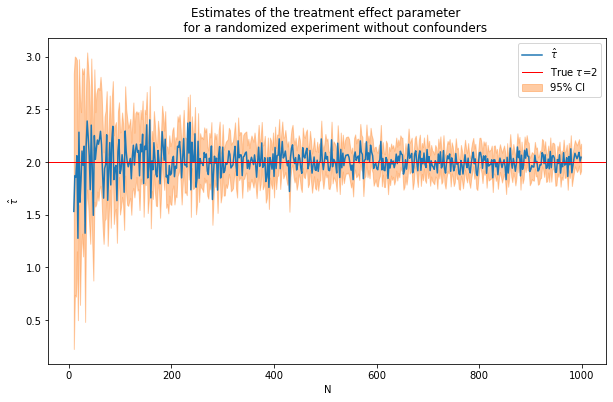

1. Experiments with no covariates in the DGP

$y_i = \tau*T_i+e_i$

tau = 2

corr = .5

conf=False # Confounder

p = 10

p0 = 0 # number of covariates used in the DGP

Nrange = range(10,1000,2) # loop over N values

(nvalues,tauhats,sehats,lb,ub) = fn_run_experiments(tau,Nrange,p,p0,corr,conf)

100%|███████████████████████████████████████████████████████████████████████████████| 495/495 [00:03<00:00, 139.44it/s]

caption = """Estimates of the treatment effect parameter

for a randomized experiment without confounders"""

fn_plot_with_ci(nvalues,tauhats,tau,lb,ub,caption)

For selected N check that this is the same as running a regression with a intercept

# Same process with fn_run_experiments

N = 100

Yexp,T = fn_generate_data(tau,N,10,0,corr,conf = False)

Yt = Yexp[np.where(T==1)[0],:]

Yc = Yexp[np.where(T==0)[0],:]

tauhat,se_tauhat = fn_tauhat_means(Yt,Yc)

# n_values = n_values + [N]

# tauhats = tauhats + [tauhat]

lb = lb + [tauhat-1.96*se_tauhat]

ub = ub + [tauhat+1.96*se_tauhat]

tauhat,se_tauhat

(2.4021370455607616, 0.19395861039288148)

# np.linalg.inv(np.transpose(T)@T)@np.transpose(T)@Yexp

const = np.ones([N,1])

model = sm.OLS(Yexp,np.concatenate([T,const],axis = 1))

res = model.fit()

# res.summary()

res.params[0], res.HC1_se[0]

(2.402137045560761, 0.1939586103928815)

Run R Monte Carlo iterations and compute bias, RMSE and size

estDict = {}

R = 2000

for N in [10,50,100,500,1000]:

tauhats = []

sehats = []

for r in tqdm(range(R)):

Yexp,T = fn_generate_data(tau,N,10,0,corr,conf)

Yt = Yexp[np.where(T==1)[0],:]

Yc = Yexp[np.where(T==0)[0],:]

tauhat,se_tauhat = fn_tauhat_means(Yt,Yc)

tauhats = tauhats + [tauhat]

sehats = sehats + [se_tauhat]

estDict[N] = {

'tauhat':np.array(tauhats).reshape([len(tauhats),1]),

'sehat':np.array(sehats).reshape([len(sehats),1])

}

100%|████████████████████████████████████████████████████████████████████████████| 2000/2000 [00:01<00:00, 1236.10it/s]

100%|████████████████████████████████████████████████████████████████████████████| 2000/2000 [00:01<00:00, 1099.63it/s]

100%|█████████████████████████████████████████████████████████████████████████████| 2000/2000 [00:02<00:00, 919.77it/s]

100%|█████████████████████████████████████████████████████████████████████████████| 2000/2000 [00:11<00:00, 172.97it/s]

100%|██████████████████████████████████████████████████████████████████████████████| 2000/2000 [00:33<00:00, 59.78it/s]

tau0 = tau*np.ones([R,1])

for N, results in estDict.items():

(bias,rmse,size) = fn_bias_rmse_size(tau0,results['tauhat'],

results['sehat'])

print(f'N={N}: bias={bias}, RMSE={rmse}, size={size}')

N=10: bias=-0.01968055225461872, RMSE=0.6433345010248737, size=0.09

N=50: bias=-0.001486741612216921, RMSE=0.2800864398714727, size=0.0505

N=100: bias=-0.009536594843188188, RMSE=0.19687551715639262, size=0.042

N=500: bias=-0.0010245711589984667, RMSE=0.0896230635454456, size=0.0475

N=1000: bias=0.0014414511411529878, RMSE=0.06482022539698959, size=0.06

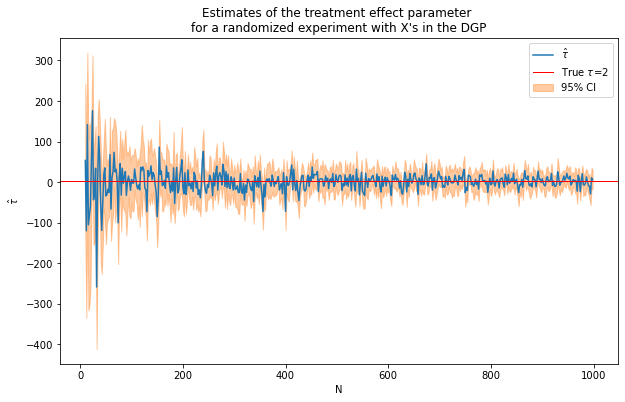

1. Experiments with covariates in the DGP

$y_i = \tauT_i+\beta`x_i+e_i$

tau = 2

corr = .5

conf=False

p = 100

p0 = 50 # number of covariates used in the DGP

Nrange = range(10,1000,2) # loop over N values

(nvalues_x,tauhats_x,sehats_x,lb_x,ub_x) = fn_run_experiments(tau,Nrange,p,p0,corr,conf)

100%|████████████████████████████████████████████████████████████████████████████████| 495/495 [00:07<00:00, 66.67it/s]

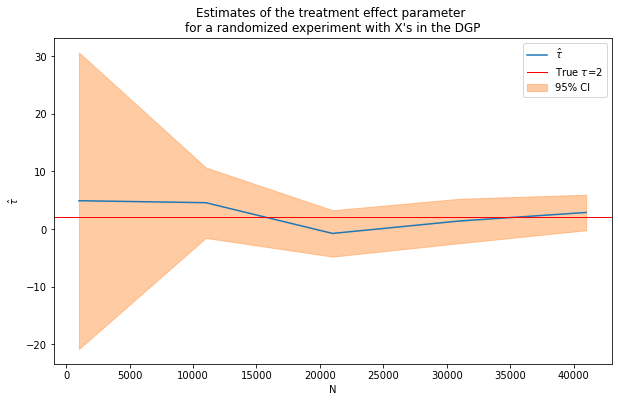

caption = """Estimates of the treatment effect parameter

for a randomized experiment with X's in the DGP"""

fn_plot_with_ci(nvalues_x,tauhats_x,tau,lb_x,ub_x,caption)

tau = 2

corr = .5

conf=False

p = 100

p0 = 0 # number of covariates used in the DGP

Nrange = range(10,1000,2) # loop over N values

(nvalues_x0,tauhats_x0,sehats_x0,lb_x0,ub_x0) = fn_run_experiments(tau,Nrange,p,p0,corr,conf)

100%|████████████████████████████████████████████████████████████████████████████████| 495/495 [00:07<00:00, 66.57it/s]

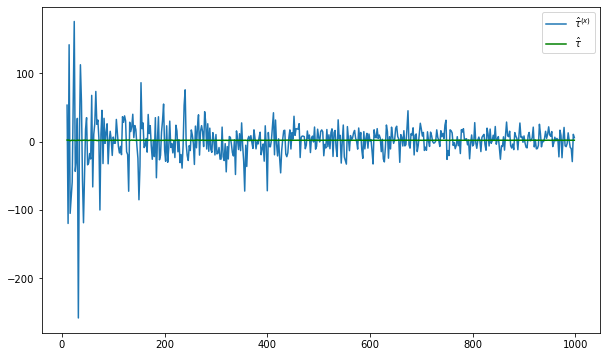

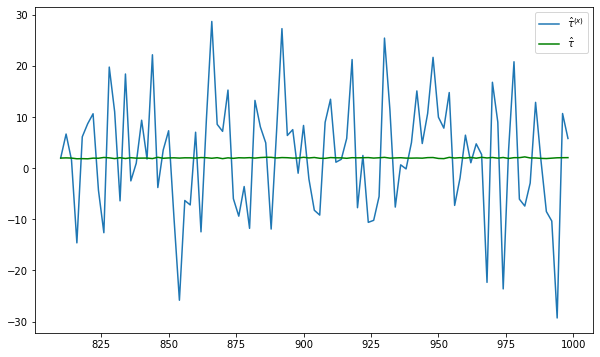

fig = plt.figure(figsize = (10,6))

plt.plot(nvalues_x,tauhats_x,label = '$\hat{\\tau}^{(x)}$')

plt.plot(nvalues_x,tauhats_x0,label = '$\hat{\\tau}$',color = 'green')

plt.legend()

<matplotlib.legend.Legend at 0x20402a931f0>

fig = plt.figure(figsize = (10,6))

plt.plot(nvalues_x[400:],tauhats_x[400:],label = '$\hat{\\tau}^{(x)}$')

plt.plot(nvalues_x[400:],tauhats_x0[400:],label = '$\hat{\\tau}$',color = 'green')

plt.legend()

<matplotlib.legend.Legend at 0x20403e4aa90>

Repeat experiment with larger N

tau = 2

corr = .5

conf=False

p = 100

p0 = 50 # number of covariates used in the DGP

Nrange = range(1000,50000,10000) # loop over N values

(nvalues_x2,tauhats_x2,sehats_x2,lb_x2,ub_x2) = fn_run_experiments(tau,Nrange,p,p0,corr,conf)

100%|████████████████████████████████████████████████████████████████████████████████████| 5/5 [00:39<00:00, 7.96s/it]

fn_plot_with_ci(nvalues_x2,tauhats_x2,tau,lb_x2,ub_x2,caption)

Still pretty noisy!

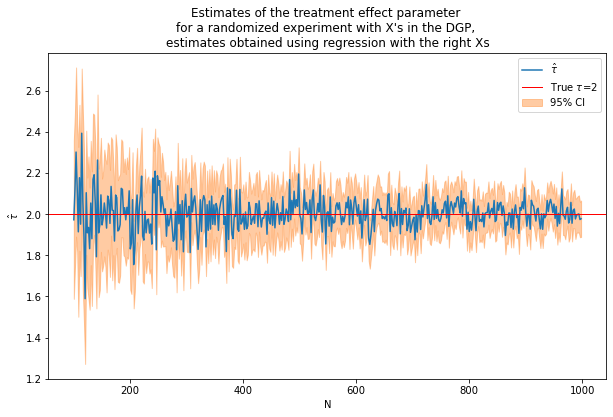

DGP with X - adding covariates to the regression

Use same DGP as before

# Use same DGP as

tau = 2

corr = .5

conf=False

p = 100

p0 = 50 # number of covariates used in the DGP

Nrange = range(100,1000,2) # loop over N values

# we need to start with more observations than p

flagX = 1

(nvalues2,tauhats2,sehats2,lb2,ub2) = fn_run_experiments(tau,Nrange,p,p0,corr,conf,flagX)

100%|████████████████████████████████████████████████████████████████████████████████| 450/450 [00:10<00:00, 43.69it/s]

caption = """Estimates of the treatment effect parameter

for a randomized experiment with X's in the DGP,

estimates obtained using regression with the right Xs"""

fn_plot_with_ci(nvalues2,tauhats2,tau,lb2,ub2,caption)

Including X’s improves precision. However, we cheated because we included the right X’s from the start!

What happens if we use some X’s that influence the outcome and some that don’t?

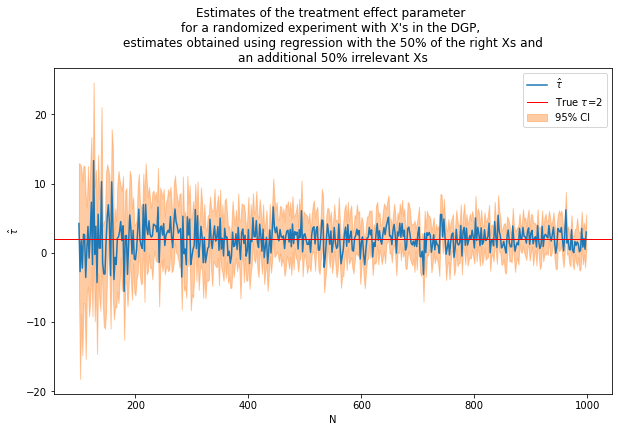

# Use same DGP as

tau = 2

corr = .5

conf=False

p = 1000

p0 = 50 # number of covariates used in the DGP

Nrange = range(100,1000,2) # loop over N values

# we need to start with more observations than p

flagX = 2

(nvalues3,tauhats3,sehats3,lb3,ub3) = fn_run_experiments(tau,Nrange,p,p0,corr,conf,flagX)

100%|████████████████████████████████████████████████████████████████████████████████| 450/450 [01:18<00:00, 5.73it/s]

caption = """Estimates of the treatment effect parameter

for a randomized experiment with X's in the DGP,

estimates obtained using regression with the 50% of the right Xs and

an additional 50% irrelevant Xs"""

fn_plot_with_ci(nvalues3,tauhats3,tau,lb3,ub3,caption)